Introduction

Banks and financial institutions are generating data faster than ever — from real-time payment streams and digital transactions to AI-driven credit decisioning and multi-jurisdictional regulatory reports. Yet most firms still run on infrastructure designed for a different era, when overnight batch runs were acceptable and data silos were an inconvenience rather than a liability.

The gap has become expensive. Banks spend 70–75% of their IT budgets maintaining legacy systems, leaving barely a quarter of available investment for anything new. That maintenance burden translates directly into compliance exposure, slower fraud response, and delayed AI adoption — all while fintech competitors operate on architectures designed from the ground up for real-time, cloud-native workloads.

This article breaks down what modern financial data infrastructure actually looks like in practice. It covers core components, the use cases it unlocks, how to build compliance in from the start, and how to modernize incrementally — without disrupting the systems your business depends on.

Key Takeaways

- Modern financial data infrastructure is modular and cloud-based, built around trusted data rather than raw volume.

- Legacy architecture creates data silos, batch-processing delays, and compounding compliance risk.

- Key use cases: real-time fraud detection, automated credit decisioning, regulatory reporting, and customer 360 analytics.

- Governance, MDM, and data quality must be embedded from day one; retrofitting them later is costly and unreliable.

- Phased migrations outperform big-bang approaches: 92% success rate vs. 58% in financial services.

Why Financial Institutions Need Modern Data Infrastructure Now

The Structural Failure Modes of Legacy Systems

Legacy architecture fails financial institutions in three specific ways:

- Siloed databases prevent unified customer and transaction views, making a true 360-degree customer profile impossible without manual reconciliation.

- Batch processing introduces dangerous windows in fraud detection and compliance monitoring — hours during which criminals can execute follow-on transactions before a detection system catches the first one.

- On-premises storage lacks the elastic compute required to run modern AI/ML workloads at scale, particularly during volume spikes.

Fraud detection latency makes the cost of legacy processing concrete. Traditional batch systems operate on cycles delayed by hours or days. Real-time streaming architectures analyze transactions in milliseconds — Apache Flink-based systems have demonstrated sub-10ms detection latency for banking use cases. By the time a batch system flags a suspicious transaction, a fraud chain may have already cleared multiple accounts.

Each of these failure modes has a direct business cost. That's what's driving financial institutions to modernize now, not at the next planning cycle.

Business Drivers Accelerating Modernization

Four pressures are pushing financial institutions toward infrastructure overhaul at the same time:

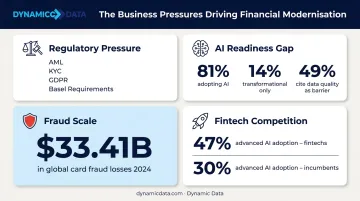

- Regulatory pressure: AML, KYC, Basel III/IV, GDPR, and e-invoicing mandates require audit-ready data at all times — not just at quarter-end.

- AI readiness gap: 81% of financial firms are adopting AI at some level, but only 14% consider it transformational — and 49% of traditional institutions cite data availability and quality as the leading barrier.

- Fraud scale: Global card fraud losses reached $33.41 billion in 2024.

- Fintech competition: Fintechs reach advanced AI adoption at 47% versus 30% for incumbents, running on architectures that incumbents are only beginning to build.

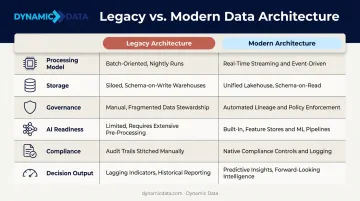

Legacy vs. Modern: A Direct Comparison

| Dimension | Legacy Architecture | Modern Architecture |

|---|---|---|

| Processing model | Nightly batch runs | Event-driven, real-time streaming |

| Storage | Siloed relational databases | Data lakehouse (unified analytics + operations) |

| Governance | Manual, after-the-fact | Embedded, automated lineage and controls |

| AI readiness | Data must be extracted and cleaned first | Feature stores, ML pipelines built in |

| Compliance | Point-in-time reports | Continuous, queryable audit trails |

| Decision output | Static dashboards | AI copilots and automated decisioning |

Core Components of a Modern Financial Data Infrastructure

Data Ingestion and Integration Layer

Modern architectures use event-driven, API-first pipelines to ingest data in real time from core banking systems, ERP platforms, payment networks, and market feeds. The integration layer must handle three distinct data types simultaneously:

- Structured transactions (account records, payment confirmations)

- Unstructured documents (loan applications, KYC documentation)

- Streaming feeds (card authorization events, market ticks)

Batch ETL pipelines cannot serve all three. A modern ingestion layer treats each as a first-class concern with appropriate tooling and latency guarantees.

Cloud-Native and Hybrid Storage (Data Lakehouse Model)

The shift from traditional data warehouses to a lakehouse model gives financial institutions something previous architectures couldn't offer: structured querying on flexible storage, without duplicating data across systems.

Open table formats — Delta Lake, Apache Iceberg, Apache Hudi — support ACID transactions on object storage, meaning institutions can run compliance queries, fraud analytics, and operational reporting against a single platform. For large institutions mid-transition, hybrid architectures (cloud plus on-premises) are a practical interim state, not a failure condition.

Data Governance and Master Data Management

MDM establishes single authoritative records for the domains that matter most in financial services: customers, accounts, and products. Without it, downstream analytics and AI models draw from inconsistent inputs — different systems disagree on what constitutes a customer record, and those discrepancies accumulate into material compliance risk.

The financial cost is documented: poor data quality costs organizations an average of $12.9 million per year, with more than 25% of organizations losing over $5 million annually (IBM, 2025). In financial services, the exposure is sharper — Equifax reached a $725,000 settlement after a legacy system error produced inaccurate credit scores at scale.

Governance cannot be bolted on after the platform is built. Dynamic Data's analytics engineering team addresses this by using dbt to enforce consistent transformation logic across financial reporting and analytics pipelines — keeping reporting tables, customer master records, and transactional aggregates aligned as source systems evolve.

Real-Time Processing Layer

Stream processing engines — Apache Kafka, Apache Flink — allow institutions to act on data as it arrives rather than waiting for overnight batch runs. Over 80% of the Fortune 100 already run Kafka as their streaming foundation. That translates directly to outcomes: millisecond-level fraud signal detection versus hours-long batch windows. For credit assessments and dynamic risk pricing, acting on stale data isn't just inefficient — it misprices risk in ways that compound over time.

AI/ML Enablement and Security Layers

Supporting production AI in financial services requires more than model training infrastructure. A compliant AI platform includes:

- Feature stores for consistent, versioned input data

- Model registries with lineage tracking and rollback capabilities

- Vector databases for unstructured data search (document-based KYC, for example)

- RBAC and audit trails that make model outputs explainable to regulators

Security controls — encryption at rest and in transit, role-based access, data residency enforcement — and observability tooling (data quality monitoring, freshness checks, lineage queries) sit alongside the AI layer as non-negotiable infrastructure. For regulated institutions, queryable audit trails are a supervisory requirement, not a best practice.

Key Use Cases Enabled by Modern Financial Data Infrastructure

Fraud Detection and Prevention

Real-time streaming combined with anomaly detection models lets institutions identify and stop fraudulent transactions before a batch window closes. Yapi Kredi achieved a 98.7% reduction in fraud losses over seven years using AI-powered real-time detection — a result that simply cannot be replicated on batch architecture, where the detection window opens after the transaction has already settled.

With global card fraud projected to reach $41 billion by 2030, real-time infrastructure is the difference between absorbing fraud losses and preventing them.

Credit Assessment and Automated Loan Decisioning

Modern infrastructure aggregates alternative signals — invoice histories, cash flow patterns, behavioral data — giving credit models access to richer, more current inputs than traditional bureau-only scoring allows.

The speed gains are significant. One European bank reduced loan approval "time to yes" from 24–48 hours to 4 minutes while cutting cost per origination by 30–40% (McKinsey). Automated underwriting systems achieve up to a 95% straight-through processing rate — processing applications at 4–8x the speed of manual review.

Regulatory Reporting and Audit Trails

Unified data lineage lets compliance teams generate accurate, on-demand reports across multiple jurisdictions — Basel III/IV, AML, KYC — without manual reconciliation across siloed systems.

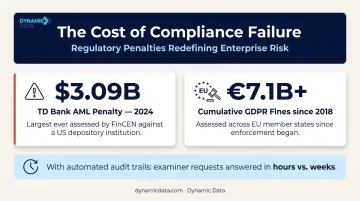

The penalty for getting this wrong has no ceiling. TD Bank received a $3.09 billion AML penalty in 2024 — the largest ever assessed against a US depository institution by FinCEN. Cumulative GDPR fines since 2018 now exceed €7.1 billion. Automated audit trails mean compliance teams can respond to examiner requests in hours rather than weeks — with full lineage tracing every data point back to its source.

Customer 360

Consolidating transaction histories, product holdings, and behavioral data into a unified customer profile enables personalized products and proactive advisory. The prerequisite is solving the identity resolution problem through MDM — fragmented legacy records make any meaningful personalization impossible without a trusted customer master.

Algorithmic Trading

Capital markets push infrastructure requirements to their limit: sub-millisecond latency, terabyte-scale ingestion, and live risk dashboards running simultaneously. At this scale, latency is a design constraint — a 10-millisecond delay in order execution can mean the difference between capturing a spread and missing it entirely.

Building a Governance-First, Regulatory-Compliant Architecture

Compliance cannot be bolted on after the fact — financial services firms that treat governance as an afterthought face regulatory penalties, audit failures, and data breaches that erode client trust. The regulatory landscape demands architecture decisions made from day one.

Key regulations shaping financial data infrastructure include:

- GDPR Article 30: Requires detailed records of all data processing activities, including purpose, categories of data, and retention periods

- BCBS 239: Mandates integrated data architecture with reliable