Key Takeaways

- 80–85% of banks lack effective strategies to use their data — the problem isn't data volume, it's structure

- Five components drive a reliable data strategy: governance, quality management, unified architecture, lineage tracking, and analytics

- Poor data quality costs organizations $12.9 million per year on average, making inaction expensive

- Cloud adoption is accelerating, yet most institutions are still in early stages; a phased approach reduces risk

- Warning signs of a failing strategy include shadow spreadsheets, manual regulatory filings, and unexplainable AI outputs

Introduction

Most financial institutions aren't short on data. They're short on the ability to use it.

Transaction records sit in core banking systems. Customer profiles are scattered across lending, deposits, and wealth management platforms. Risk metrics live in spreadsheets that three different analysts maintain separately, producing three different answers.

The result? Major decisions still get made on gut instinct, outdated reports, or whichever number got to the boardroom first.

According to BizTech Magazine, between 80%–85% of banks lack effective strategies to use their data. That's not a technology gap. It's a strategy gap.

This article covers:

- What a reliable data strategy actually looks like in financial services

- Why most strategies fail before delivering value

- The five components that make one work

- How to recognize when yours needs reinforcement

What a Data Strategy Does in Financial Services

Having data and having a plan for it are two completely different things.

A data strategy defines how an institution collects, stores, governs, and activates its data to support business decisions — not just regulatory reporting. Without one, data efforts default to compliance documentation rather than the infrastructure needed for faster credit decisions, better customer engagement, and AI outputs teams can actually trust.

From Reactive to Decision-Ready

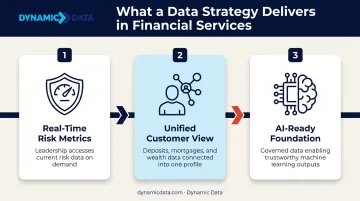

In financial services specifically, a data strategy does three things that general data management doesn't:

- Gives leadership access to current, reliable risk metrics when they need them — not last quarter's exposure pulled after the fact

- Connects deposits, mortgages, and wealth management data into a single customer view, so teams understand the full relationship rather than a single product

- Creates the foundation for AI adoption — machine learning models are only as reliable as the data they're trained on, and without a strategy, those initiatives stall or produce results no one trusts

Built to Evolve, Not Just to Launch

A data strategy is not a one-time project. Regulations change. New products get added. Architectures that worked at 10 million transactions per day don't work at 100 million. The institutions that get the most from their data treat strategy as an ongoing framework that adapts, not a document they finalize once and shelve.

Why Financial Services Data Strategies Fall Short

Siloed, Product-Centric Architecture

Most financial institutions were built product by product. Lending got its own system. Deposits got another. Wealth management a third. Each system created its own customer record — often with different name formats, inconsistent identifiers, and missing fields.

The result is structurally impossible to unify without deliberate remediation. You can't build a reliable view of the customer relationship when the customer exists as three different records across three different systems.

Legacy Technology Debt

Older core banking systems were built under storage constraints that no longer exist — but their data still carries the scars. Truncated fields. Years of transaction history locked in systems that weren't designed for modern analytics extraction. Only 7% of core banking workloads have been migrated to the cloud globally, making this the single biggest bottleneck for downstream analytics and AI initiatives.

The Culture Gap

Many institutions still treat data strategy as an IT initiative. Without executive sponsorship and cross-functional ownership, projects lose momentum, governance frameworks go unenforced, and priorities shift with each leadership change. A 2021 Exasol survey found 70% of enterprises lack a mature data strategy — and financial services firms are not exempt from that pattern.

The Governance Deficit and Its Downstream Cost

Without clear data ownership, quality degrades quietly — often for years before anyone notices. Common symptoms include:

- Duplicate records accumulating across systems

- Metric definitions drifting between teams

- Transformations left undocumented and untraceable

By the time the problem surfaces — usually during a regulatory filing or a model review — it has already compounded.

This matters most when AI enters the picture. Unreliable training data produces unreliable outputs. Before any institution can meaningfully deploy machine learning, it needs traceable, validated data to build on. Data quality isn't a prerequisite for analytics alone — it's a prerequisite for AI adoption entirely.

The 5 Essential Components of a Data Strategy in Financial Services

Component 1: Data Governance Framework

Governance defines who owns the data, what standards apply, and how quality is enforced over time. It operates across three pillars:

- People — data stewards, business owners, and steering committees who hold accountability

- Process — creation policies, provisioning rules, and quality gates that standardize how data moves through the organization

- Technology — systems that enforce and monitor governance automatically, rather than relying on periodic audits

Governance is what keeps the other four components functional after implementation. Without it, architecture decays, data quality erodes, and the entire framework unravels — no matter how well the rest was built.

Component 2: Data Quality Management

Gartner research found that poor data quality costs organizations at least $12.9 million per year on average. In financial services, the stakes are higher — Citigroup was fined $136 million for unresolved data management failures, and JPMorgan's 2012 "London Whale" incident resulted in a $6 billion loss linked to risk data aggregation failures.

Active data quality management requires:

- Data profiling — understanding the current state of each data domain

- Quality analysis — identifying gaps in completeness, accuracy, consistency, and timeliness

- Quality criteria by domain — financial, operational, and regulatory data each have different tolerances

- Continuous monitoring — automated alerts when data falls below defined thresholds

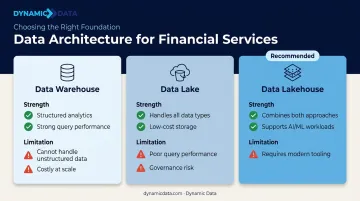

Component 3: Unified Data Architecture

Breaking down silos requires a centralized platform where data from disconnected systems can be standardized, enriched, and made accessible across teams. The data lakehouse architecture has become the preferred approach for financial services — combining the flexible, low-cost storage of a data lake with the structured querying and governance features of a data warehouse.

The table below compares the three main architectural options:

| Architecture | Strengths | Limitations |

|---|---|---|

| Data Warehouse | Structured analytics, strong query performance | Cannot handle unstructured data; costly at scale |

| Data Lake | Handles all data types, low-cost storage | Poor query performance; governance risk |

| Data Lakehouse | Combines both, supports AI/ML workloads | Requires modern tooling and expertise |

Running traditional analytics and AI workloads from a single platform eliminates the data movement overhead that separate architectures create — reducing latency, cost, and governance complexity at once.

Component 4: Data Lineage and Metadata Tracking

Every input, transformation, and output must be documented. In regulated environments, this isn't optional — it's the mechanism that makes audits manageable and AI outputs defensible.

When an examiner asks where a risk figure came from, the answer needs to trace back through every transformation to its source. Institutions without lineage tracking spend weeks reconstructing that answer manually. Those with lineage in place respond in hours.

Component 5: Analytics and Visualization Layer

The final component converts governed, high-quality data into decisions. Dashboards, scheduled reports, and predictive models make data accessible to non-technical decision-makers — risk officers, compliance teams, and relationship managers — without requiring direct database access.

Platforms like Power BI, Tableau, Looker, and Sigma each serve different organizational needs. The right choice depends on the institution's technical environment, reporting frequency requirements, and the technical fluency of end users. Selecting the wrong platform creates adoption problems that undermine the entire analytics investment — so evaluation should happen before implementation, not after.

Data Governance: The Backbone of Trustworthy Decision-Making

If the data architecture is the engine, governance is the maintenance system. Skip maintenance long enough, and the engine fails — quietly, through small failures that compound until something breaks at the worst possible moment.

What Shared Ownership Looks Like

Governance cannot live exclusively in IT. Business units, compliance, and engineering must collaborate to define what "clean" means for each data domain, set quality thresholds, and own the process of flagging anomalies when they appear.

This cross-functional model is what separates reactive institutions from resilient ones. When compliance owns the definition of a "compliant customer record" and engineering owns the pipeline that produces it, both teams are directly accountable for the result.

The CDO's Role

The Chief Data Officer role in financial services emerged post-2008 as a defensive, compliance-driven position — and according to MIT Sloan, it's still evolving toward strategic value creation. The most effective CDOs build governance into daily workflows rather than enforcing it through periodic audits. That shift — from reactive auditing to continuous accountability — is what makes governance a competitive asset rather than a compliance burden.

Governance and Regulatory Confidence

That same governance maturity translates directly into audit outcomes. Institutions that can produce accurate, traceable data on demand respond to regulatory inquiries efficiently. Those without governance infrastructure spend weeks compiling reports that still contain inconsistencies — exactly the pattern regulators have documented at scale.

BCBS 239 — the Basel Committee's principles for risk data aggregation — was issued in 2013, with compliance expected by 2016. A 2023 progress report from the Basel Committee found that "significant work remains at most banks to fully adopt the Principles." Nearly a decade after the compliance deadline, the governance gap in financial services remains real and measurable.

What a Data Platform Strategy Looks Like in Practice

A data platform strategy is the technical blueprint that governs how data is ingested, stored, processed, and made accessible. For financial institutions, it must handle high transaction volumes, strict security and compliance requirements, and the need for real-time analytics.

The 5 Layers of a Modern Data Platform

| Layer | Function |

|---|---|

| Ingestion | Collecting data from source systems — core banking, CRM, market feeds, third-party providers |

| Storage | Persisting data in lakes, warehouses, or lakehouses with appropriate access controls |

| Processing | Transforming, cleaning, and enriching raw data through ETL/ELT pipelines |

| Analytics / Serving | Delivering insights via dashboards, APIs, and ML models to business users |

| Governance / Orchestration | Managing metadata, lineage, data quality, security, and workflow automation |

Each layer depends on the ones below it. A sophisticated analytics layer built on poorly governed storage produces untrustworthy outputs — a pattern that shows up repeatedly in institutions where data quality was never addressed at the foundation.

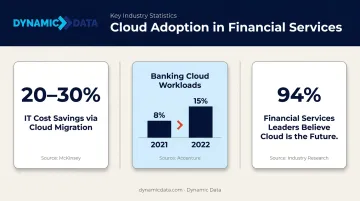

Why Cloud Adoption Is Accelerating

Cloud platforms have changed the economics of data infrastructure. The numbers reflect a clear shift:

- McKinsey estimates financial institutions can realize 20–30% cost savings on IT infrastructure through successful cloud migration

- Banking cloud workloads nearly doubled from 8% to 15% between 2021 and 2022, per Accenture data

- 94% of financial services leaders now believe cloud is the future of IT operations

Cloud has effectively democratized enterprise-grade data infrastructure. Institutions no longer need the budgets of the largest global banks to access the same capabilities — platforms like Snowflake, BigQuery, Databricks, and AWS have made that a realistic option at any scale.

Building that stack requires expertise across data engineering, modeling, and visualization. Dynamic Data helps financial services firms design and implement modern data stacks: from pipeline automation using tools like dbt and Fivetran to BI dashboards in Tableau, Power BI, or Sigma, all built around their specific compliance and reporting requirements.

Warning Signs Your Data Strategy Needs Reinforcement

These patterns show up repeatedly in institutions where the strategy has stalled or was never fully implemented.

Operational Red Flags

- Shadow spreadsheets — teams maintain their own data files because they don't trust centralized reports

- Manual regulatory filings — compliance teams spend weeks compiling reports that should take hours

- Decisions made without data — pulling the relevant information takes longer than making the call without it

Each of these points back to structural gaps — in architecture, governance, or both — not individual team failures.

Technical Red Flags

- AI or analytics outputs that cannot be explained or traced back to source data

- Data pipelines with no monitoring or alerting — failures go undetected until they cause downstream errors

- QA processes that test code functionality but skip data validation entirely

Technical flags are dangerous precisely because they stay invisible until something breaks in production. A risk model returns wrong outputs. A regulatory filing contains incorrect figures. An AI recommendation can't be explained to an examiner.

What These Signals Mean

Institutions recognizing multiple flags from either list have shifted into reactive mode. The cost of staying there compounds: data volumes increase, regulations tighten, and competitors build infrastructure that supports faster, more confident decisions.

These warning signs are a prioritization signal. The institutions that address them systematically tend to move from firefighting to building infrastructure that actually holds.

Frequently Asked Questions

What are the 5 essential components of a data strategy?

The five components are data governance, data quality management, unified data architecture, data lineage and metadata tracking, and an analytics/visualization layer. All five must work in concert: strong architecture with weak governance degrades over time, and quality data without visualization never reaches decision-makers.

What does a data strategy do?

A data strategy defines how an organization collects, governs, and activates its data to achieve business outcomes. In financial services, this means enabling faster decisions, reducing compliance risk, and building the infrastructure that makes AI adoption viable.

What is the data strategy for financial services?

Financial services data strategy must balance business intelligence, regulatory compliance, and customer insight simultaneously. It requires unified data architecture, strong governance with clear ownership, and traceable lineage because in regulated environments, provenance is as critical as the data itself.

What is a data platform strategy?

A data platform strategy is the technical blueprint governing how data is ingested, stored, processed, and made accessible across an organization. For financial institutions specifically, it must handle high transaction volumes, meet strict security and compliance requirements, and support real-time analytics at scale.

What are the 5 layers of a data platform?

The five layers are ingestion (collecting data from source systems), storage (persisting it in lakes, warehouses, or lakehouses), processing (transforming and enriching raw data), analytics/serving (delivering insights to users and models), and governance/orchestration (managing metadata, lineage, quality, and workflows).

What are the 5 C's of data governance?

The "5 C's" is a practitioner shorthand, not a formally standardized framework, typically covering Completeness, Consistency, Currency, Conformity, and Correctness. DAMA UK's authoritative model defines six dimensions: Completeness, Uniqueness, Timeliness, Validity, Accuracy, and Consistency. For financial services, DAMA's framework is the more defensible choice in audit and compliance contexts.