Fintechs face a uniquely exposed threat surface. Neobanks, crypto platforms, digital lenders, and payment apps operate at speed and scale with minimal physical friction — which means fraud can propagate faster than a human analyst can respond. Real-time, data-intelligent detection isn't a nice-to-have; it's infrastructure.

This guide cuts through the vendor noise to spotlight five fraud detection platforms purpose-built for fintech in 2026, plus the evaluation criteria your team should apply before committing.

Key Takeaways

- Synthetic identities, account takeovers, and money mule networks require ML-native platforms; rule-based systems simply can't adapt fast enough

- The five platforms reviewed (Sardine, Feedzai, ComplyAdvantage, SEON, and BioCatch) each address different fintech fraud vectors

- Selection criteria that matter most: real-time detection latency, false positive rates, API flexibility, explainability, and AML/KYC coverage

- All pricing is custom or usage-based — request demos and pilot against your own fraud data before committing

Fintech Fraud Detection in 2026: What You're Actually Up Against

Fintech fraud detection is the continuous, real-time process of identifying suspicious activity — unauthorized transactions, synthetic onboarding attempts (fake identities built from real data fragments), session hijacking — across digital financial services. It's distinct from broader fraud prevention (which includes policy and controls design) and post-incident management (which is reactive). Detection happens during the event, not before or after.

The 2026 Threat Landscape

The barrier to fraud has dropped sharply. AI tools now let bad actors generate convincing fake identities, automate credential stuffing at scale, and script social engineering attacks with minimal effort. Akamai's research counted 26 billion credential stuffing attempts every month, up nearly 50% in 18 months. Deepfake fraud attempts have increased over 2,000% in three years.

Fintechs running legacy rule-based systems are caught flat-footed. These systems require months of historical data before models can be retrained — and real-time payment rails like FedNow and SEPA don't wait.

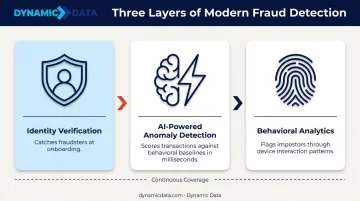

Effective fraud detection in 2026 layers three capabilities:

- Identity verification — catches fraudsters at onboarding, before they're inside the system

- AI-powered anomaly detection — scores every transaction against behavioral baselines in milliseconds, not minutes

- Behavioral analytics — flags impostors through device interaction patterns, even when stolen credentials check out

The platforms below were selected for their depth across all three layers — with particular weight on real-time detection and coverage of AI-enabled fraud vectors.

Top Fintech Fraud Detection Platforms in 2026

These five platforms were chosen for their fintech relevance, detection sophistication, integration flexibility, and ability to address the fraud vectors most common to digital financial services — not simply for brand recognition.

Sardine

Background: Sardine describes itself as a behavior-infused fraud and compliance platform built specifically for fintech, crypto, and digital banking. It covers the full customer lifecycle — from onboarding and login through payments and ongoing account monitoring — combining device intelligence with behavioral biometrics.

Why it stands out: Sardine's differentiator is its DIBB (Device Intelligence & Behavior) signal architecture, enriched with data from external providers spanning phone, email, SSN, and banking sources. This lets it surface fraud before transactions complete. Its Sonar consortium network connects signals across fintech, banking, and commerce, exposing fraud patterns no single organization sees alone. The platform also unifies AML, KYC, and fraud detection in a single API-first stack: a meaningful advantage for fintechs managing multiple compliance obligations under one integration.

Sardine raised $70 million in Series C funding in February 2025 and counts Nubank, Gusto, Deel, and bunq among its named customers.

| Category | Details |

|---|---|

| Best For | Lifecycle fraud detection, AML/KYC compliance, crypto payment fraud, money mule and ATO prevention |

| Key Features | Real-time ML + rules engine; device + behavioral biometric signals; Sonar consortium network; modular API-first architecture; transparent, explainable models |

| Pricing | Custom — contact Sardine directly |

Feedzai

Background: Feedzai is an AI-based fraud management platform designed for banks, payment providers, and fintechs. It continuously profiles user behavior, establishes baselines for normal activity, and scores every transaction via its TrustScore system using behavioral patterns, device intelligence, and network-wide signals.

Why it stands out: Feedzai's RiskOps framework brings data ingestion, transaction scoring, and alert management into one platform — enabling real-time decisions that balance detection accuracy with minimizing false positives.

TrustScore is built on federated learning through Feedzai IQ, processing millions of data points in milliseconds without exposing raw customer data across institutions. The platform protects over 1 billion consumers globally and has received the highest possible Forrester scores in model building, data integration, and behavioral profiling.

For fintechs managing high transaction volumes with complex fraud and scam scenarios, Feedzai's enterprise scale and explainable AI alerts make it a reliable operational foundation.

| Category | Details |

|---|---|

| Best For | Banking and neobank fraud management, real-time payment monitoring, ATO and mule detection, high-volume fintech environments |

| Key Features | Dynamic TrustScore AI scoring; RiskOps unified platform; behavioral profiling with device/biometric data; explainable alerts; scam and inbound/outbound payment monitoring |

| Pricing | Enterprise commercial — contact Feedzai directly |

ComplyAdvantage

Background: ComplyAdvantage is an AI-driven fraud and AML compliance platform. Its Mesh platform covers customer screening, transaction monitoring, payment screening, sanctions and watchlists, PEPs, and adverse media — spanning both monetary transactions and non-financial events like logins and profile changes.

Why it stands out: ComplyAdvantage's machine learning models use dynamic thresholds that auto-adjust as crime trends shift, removing the manual retraining burden that slows most compliance teams. Its identity clustering and graph network analysis traces fund flows and links accounts controlled by the same actor — a critical capability for fraud ring detection. The platform was recognized in Forrester's inaugural Financial Crime Management Solutions Landscape (Q1 2026) and has held the G2 AML Leader position for nine consecutive quarters.

For fintechs with regulatory reporting obligations — SAR filing, sanctions screening, adverse media — ComplyAdvantage provides the compliance infrastructure that pure fraud detection tools don't.

| Category | Details |

|---|---|

| Best For | AML compliance, transaction and sanctions screening, fraud ring detection, fintech regulatory reporting |

| Key Features | Dynamic ML thresholds; identity clustering and graph network analysis; Mesh unified platform; explainable alerts; built-in case management and dashboard reporting |

| Pricing | Commercial — contact ComplyAdvantage directly |

SEON

Background: SEON is a fraud prevention platform that builds digital footprint profiles from 900+ first-party signals — email, phone number, IP address, device hardware, OS, and behavioral markers — to expose fake or synthetic identities before a transaction or account creation completes.

Why it stands out: SEON takes a "whitebox" AI approach, meaning fraud teams can see exactly why a risk score was triggered, suggest rule logic from past patterns, and manually fine-tune detection with minimal technical overhead. For teams that must explain scoring decisions to compliance reviewers or regulators, that visibility is directly useful. SEON expanded its AI capabilities in September 2025, adding features that cut manual review time for fraud and AML teams.

It's particularly well-suited for onboarding fraud and multi-accounting detection . Synthetic identity fraud accounts for up to 80% of new account fraud, making these the highest-impact use cases.

| Category | Details |

|---|---|

| Best For | Onboarding fraud, synthetic identity detection, multi-accounting prevention, AML checks, registration and login fraud |

| Key Features | 900+ signal digital footprinting; device intelligence with hardware and behavioral markers; whitebox AI with explainable outputs; prebuilt rule library; real-time API-first deployment |

| Pricing | Tiered and usage-based — verify current plans on SEON's website |

BioCatch

Background: BioCatch is a behavioral biometrics platform that builds detailed user profiles from how people physically interact with their devices — analyzing over 2,000 behavioral parameters per session, including mouse movements, typing cadence, swiping patterns, and hesitation moments — to verify genuine users and flag impostors even when credentials are correct.

Why it stands out: BioCatch operates continuously from login to logout, catching threats that bypass traditional controls entirely: account takeover, mule accounts, social engineering scams, and Remote Access Trojans (RATs). RAT-related fraud increased 55% in H1 2025 compared to the prior year. Three of the four largest U.S. banks by assets now use BioCatch, and it crossed $100 million ARR with 49% growth.

Its investigation toolset goes beyond what most behavioral biometrics vendors offer:

- BioCatch Scout — fraud network link analysis and visualization

- Analyst Station — session-level video reconstruction for investigations

- Rule Manager — policy simulation before live deployment

| Category | Details |

|---|---|

| Best For | Account takeover defense, mule account detection, social engineering and scam prevention, continuous session authentication |

| Key Features | 2,000+ behavioral parameters per session; continuous login-to-logout monitoring; mule and RAT detection; BioCatch Scout network visualization; Rule Manager for policy simulation |

| Pricing | Commercial — contact BioCatch directly |

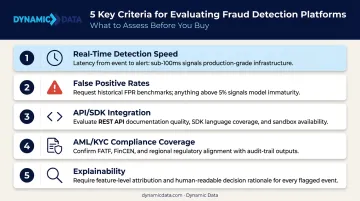

How to Evaluate These Platforms

The most common mistake fintech teams make is selecting a vendor based on brand recognition rather than assessing whether it addresses the specific fraud vectors affecting their product and customer base. A crypto exchange deals primarily with wallet takeovers and wash trading; a digital lender is more exposed to synthetic identity fraud and income misrepresentation — and the right platform for one is rarely the right fit for the other.

The factors below cut through the marketing noise and focus on what actually determines fit.

Key Evaluation Factors

| Factor | What to Assess |

|---|---|

| Real-time detection speed | Latency at transaction scoring — can it keep pace with instant payment rails? |

| False positive rates | Up to 95% of AML alerts are false positives industry-wide; a 15% loss in customer lifetime value follows from excessive friction |

| API/SDK integration | Whether it connects cleanly to your existing data pipelines, warehouses, and reporting tools |

| AML/KYC compliance coverage | Essential for regulated environments, especially post-UK APP fraud reimbursement scheme |

| Explainability | GDPR requires explaining automated decisions; audit-ready models reduce regulatory exposure |

Pricing Reality

All five platforms use custom or usage-based pricing. True cost depends on transaction volume, fraud type coverage, and compliance requirements. Before committing:

- Request a demo using scenarios relevant to your fraud types

- Run a pilot against your own historical fraud data to benchmark detection accuracy

- Confirm that data outputs integrate cleanly with your existing data warehouse and reporting infrastructure

Conclusion

Fraud in fintech is no longer a static threat managed by threshold rules and batch reviews. It evolves continuously — trained on real transaction data, exploiting gaps in legacy rule engines before teams can respond. The platforms reviewed here — Sardine, Feedzai, ComplyAdvantage, SEON, and BioCatch — represent where the detection standard sits in 2026: real-time, explainable, and purpose-built for the compliance and velocity demands of digital financial services.

When evaluating options, look beyond current detection capabilities. Assess long-term scalability, compliance alignment, and whether the platform's data outputs integrate cleanly with your existing pipelines. The right choice produces signals your fraud and risk teams can act on — not just alerts that require manual triage.

Choosing the right fraud platform solves only half the problem. The other half is making sure those detection signals flow into the reporting infrastructure, dashboards, and ML pipelines where your team actually works. That's where Dynamic Data comes in — helping fintech organizations build the data engineering layer that turns raw fraud signals into usable business intelligence. Working across Snowflake, BigQuery, Databricks, dbt, and tools like Tableau and Looker, the team builds the data engineering and visualization layer that turns raw fraud signals into business intelligence. Get in touch to discuss how Dynamic Data can help you get full operational value from whichever fraud platform you deploy.

Frequently Asked Questions

How do you detect financial fraud?

Financial fraud is detected by continuously monitoring transactions, user behavior, and identity signals using rule-based systems, machine learning models, and behavioral analytics. Anomalies — unusual transaction amounts, device mismatches, atypical login behavior — are flagged for automated blocking or human review in real time.

What is fraud detection in fintech?

Fintech fraud detection is the real-time process of identifying unauthorized or deceptive activity — account takeovers, synthetic identity onboarding, payment fraud — within digital financial services. It uses AI, behavioral biometrics, and device intelligence to catch threats before financial or reputational damage occurs.

Which technology is commonly used for fraud detection in fintech?

Core technologies include supervised and unsupervised machine learning models, behavioral biometrics, device fingerprinting, graph and network analysis, and real-time transaction scoring. Leading platforms combine several of these into a single risk decision engine rather than relying on any one method.

How do you prevent digital payment fraud?

Effective prevention combines multi-factor authentication, real-time anomaly detection, device intelligence at onboarding, velocity checks, and AML/KYC controls. These layers work best when applied continuously across the full customer lifecycle, not only at the point of payment.

What are the 4 P's of spotting fraud?

The 4 P's are:

- Profile — baseline of normal user behavior

- Patterns — deviations from that baseline

- Presence — verifying the person is who they claim to be

- Prevention — blocking or escalating suspicious activity before harm occurs

Modern platforms apply all four in parallel, in real time.