Introduction

A database that slows down by 200 milliseconds might be an inconvenience in most industries. In financial services, it can mean a failed trade execution, a fraud alert that fires too late, or a compliance report that misses its regulatory deadline.

Financial databases operate under pressures most other industries don't face:

- Real-time transaction processing at scale

- Concurrent peak loads during market open and close

- Strict audit trail requirements under regulations like SEC Rule 17a-4

- Data volumes that keep compounding from market feeds, transaction records, and regulatory mandates

According to Splunk's research, the average annual downtime cost for financial services organizations is $152 million per firm — making database performance resilience a board-level concern, not just an IT priority.

This guide covers the tuning techniques that matter most in financial contexts, the structural challenges that generic guidance overlooks, and a practical maintenance schedule built around financial operating rhythms — including early warning signs your database needs attention.

Key Takeaways

- Database performance tuning in financial services means optimizing queries, indexing, partitioning, and resource allocation to meet strict speed and reliability requirements.

- Poor performance costs financial institutions customers, revenue, and regulatory standing — and proactive maintenance is consistently cheaper than emergency fixes.

- Core techniques: query optimization, strategic indexing, data partitioning, connection pooling, and in-memory caching.

- Financial databases face unique challenges: legacy system integration, compliance overhead, data volume growth, and unpredictable peak loads.

- Sustained performance requires a structured tuning cadence, from daily monitoring through annual architecture reviews.

Why Database Performance Tuning Matters in Financial Services

Financial services operate in a near-zero-tolerance performance environment. Customer-facing apps, trading platforms, and fraud detection systems all depend on sub-second database responses — and when they don't get them, the consequences are measurable.

Trading Latency Is a P&L Issue

For trading platforms, database latency isn't a technical metric — it's a revenue variable. TABB Group research estimated that a 5-millisecond latency disadvantage can cost brokers at least 1% of order flow, valuing the impact at approximately $4 million per millisecond under typical institutional commission pools.

Every millisecond of unnecessary database overhead in order verification, balance checks, or position updates translates directly to competitive disadvantage.

Customer Retention Depends on Digital Performance

Financial customers switch providers when digital experiences disappoint. The J.D. Power 2026 U.S. Retail Banking Satisfaction Study found that 20% of consumers moved money away from their primary bank in the prior quarter, up from 17% previously. Slow app response — driven by sluggish database performance — is a primary driver of that primacy risk (the risk of losing a customer's primary banking relationship).

Compliance Reporting Runs on the Same Infrastructure

Regulatory filings, audit trails, and risk exposure calculations run on the same database infrastructure as customer-facing applications. Under SEC Rule 17a-4, broker-dealers must preserve electronic records for 3–6 years with 2 years immediately accessible. When database performance degrades, it threatens both reporting deadlines and data retrieval reliability under audit.

Reactive Fixes Cost Significantly More

Proactive tuning costs a fraction of emergency incident response. According to IBM's Systems Sciences Institute, fixing a defect after production deployment costs 6–100x more than addressing it during development — a ratio that applies directly to database performance issues left unresolved until they cause outages.

The gap compounds quickly when you factor in business impact:

- Unplanned downtime carries average costs of $5,600 per minute, per Gartner estimates

- Emergency database remediation typically requires senior DBA time at premium rates

- Regulatory reporting failures triggered by outages can add penalty exposure on top of recovery costs

Planned maintenance windows eliminate the premium entirely.

Key Database Performance Tuning Techniques for Financial Services

Financial workloads combine high-frequency writes (transactions) with complex analytical reads (reporting, risk calculations) — often simultaneously on the same infrastructure. Matching the right tuning technique to each workload type is where real performance gains are won.

Query Optimization

Poorly written SQL is among the most common causes of performance degradation in financial applications. Queries that join large tables — accounts, transactions, instruments, positions — without proper optimization can trigger full table scans that consume disproportionate resources.

Tools like EXPLAIN ANALYZE (PostgreSQL) or SET STATISTICS IO ON (SQL Server) expose exactly where queries are inefficient: which joins are unoptimized, which predicates are missing index support, and where estimated versus actual row counts diverge dramatically.

Two practices matter especially in high-transaction financial environments:

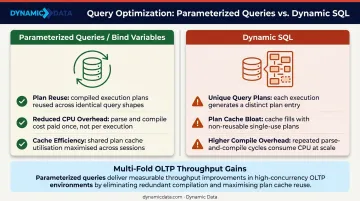

- Use parameterized queries instead of dynamic SQL — dynamic SQL generates unique query plans that can't be reused, causing plan cache bloat and higher CPU overhead on every execution. Microsoft's guidance on

sp_executesqland Oracle's bind variable best practices reach the same conclusion: parameterization enables plan reuse and reduces compile overhead at scale. - Standardize bind variables — Oracle benchmarks show that eliminating hard parses through bind variables delivers multi-fold throughput improvements in concurrent OLTP workloads. For financial systems processing thousands of transactions per second, this is foundational.

Strategic Indexing

Indexes allow the database engine to locate records without scanning entire tables — critical when transaction tables contain billions of rows. The challenge in financial databases is balance: too few indexes slow reads; too many slow writes, which is directly problematic in high-frequency transaction environments.

Composite indexes are particularly valuable for financial query patterns. A fraud detection query filtering on account_id + transaction_date + transaction_type benefits far more from a composite index on those three fields than from three separate single-column indexes.

Index strategy should be regularly reviewed against actual query patterns — an index that was optimal 18 months ago may no longer reflect current access behavior as data volumes and query patterns evolve.

Data Partitioning for Financial Datasets

Financial databases accumulate massive historical datasets: years of transaction records, market data feeds, and audit logs. Without partitioning, queries must scan entire tables even when they only need recent data.

Partitioning divides large tables into smaller, manageable segments — typically by date range for financial data. A query for last month's transactions scans only the relevant partition rather than the full transaction history.

Time-based partitioning works well for financial time-series data — market prices, transaction histories, settlement records — because date filters appear in nearly every query. Partition pruning means the query optimizer eliminates irrelevant partitions before execution even begins.

Connection Pooling and Resource Management

Financial applications experience sharp, predictable traffic spikes: market open, payday cycles, quarter-end processing. Without connection pooling, opening a new database connection per request creates significant overhead under concurrent load.

Connection pooling reuses existing connections, cutting per-request overhead during peak periods. Oracle's Universal Connection Pool guidance recommends sizing pools relative to CPU core counts and enabling statement caching to further reduce parse overhead. For PostgreSQL environments, tools like PgBouncer serve a similar function.

Memory allocation deserves equal attention. Properly sized buffer pools keep frequently accessed data pages in memory rather than on disk, which matters particularly when large analytical queries run alongside transactional workloads during business hours.

Caching for Frequently Accessed Financial Data

In-memory caching tools like Redis or Memcached are well-suited to financial data that is read far more often than it changes: exchange rates, account balance summaries, risk thresholds, reference data for instruments or counterparties.

Storing this data in memory eliminates repeated database round-trips and cuts response times substantially — Redis engineering guidance for payment processing contexts cites end-to-end targets of 100–200 ms for authorization, with fraud scoring budgets as low as 10–50 ms.

One financial-specific consideration: TTL (time-to-live) settings must be calibrated carefully. Treating all cached data identically is a common configuration mistake. TTL requirements vary significantly by data type:

- Account balances — require aggressive expiry to prevent serving stale figures

- Market data and rates — short TTLs aligned to update frequency (seconds to minutes)

- Static reference data — instrument metadata, regulatory thresholds can tolerate longer TTLs

Financial-Specific Performance Challenges That Demand Tuning Attention

Generic tuning guidance doesn't fully account for the structural challenges financial databases face. These are the ones that surface most frequently in practice.

Legacy System Integration Latency

Many financial institutions run hybrid environments where modern applications interface with legacy core banking or trading systems through translation layers. These integration points add latency that compounds database performance problems — a query that runs in 50ms internally can take 300ms end-to-end when it must transit a legacy API layer.

Strategies that help include read replicas (offloading reporting queries from the primary transactional system), API caching at the integration boundary, and schema alignment work that reduces data transformation overhead between systems.

Compliance and Security Overhead

Financial databases carry significant security requirements: transparent data encryption, role-based access controls, and comprehensive audit logging. These aren't optional, but they do consume processing resources.

Peer-reviewed testing of Transparent Data Encryption shows measurable overhead, though AES hardware acceleration largely offsets the performance penalty. Audit logging impact can be managed through:

- Asynchronous logging: write audit records to a buffer rather than synchronously to disk on every transaction

- Partitioned audit tables: keep audit data in its own partitioned structure, preventing audit volume from degrading operational query performance

Data Volume Growth

Financial institutions generate data at rates that stress operational databases over time. Global market data spend reached $44.3 billion in 2024, reflecting the scale of data flowing through financial infrastructure.

The structural solution is separating analytical and operational workloads. Well-architected dbt pipelines move historical and analytical data to purpose-built platforms like Snowflake or BigQuery, freeing transactional databases from the weight of multi-year historical analyses running alongside live transaction processing. Dynamic Data regularly implements this architecture for financial services clients.

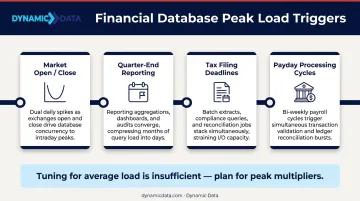

Peak Load Management

Financial databases face highly concentrated traffic. Common peak triggers include:

- Market open and close periods (a well-documented U-shaped intraday volume pattern)

- Quarter-end reporting runs

- Tax filing deadlines

- Payday processing cycles

Tuning for average load is insufficient. Capacity planning must account for peak multipliers, and auto-scaling strategies should be tested against realistic peak scenarios — not just typical daily throughput.

Warning Signs Your Financial Database Needs Tuning

Most database performance problems announce themselves gradually before they become crises. These are the leading indicators to watch.

Performance Metric Drift

- Query response times creeping above acceptable thresholds (sub-200ms for customer-facing apps, sub-second for fraud detection)

- CPU or memory utilization rising during what should be normal workloads

- Growing disk I/O wait times — particularly if they correlate with specific query types

By the time end users notice, the underlying problem has typically been building for weeks.

Transaction Failures and Timeouts

An increase in timed-out transactions, connection errors, or failed batch jobs during peak periods indicates the database is operating beyond its optimized capacity. In financial services, the downstream effects are immediate:

- Failed customer actions during high-traffic windows

- Delayed settlement processing that cascades into reconciliation errors

- Interrupted reporting runs that require manual restarts and validation

Compliance Reporting Delays

A nightly or monthly reporting job that now takes 40% longer than it did six months ago signals accumulated performance degradation — index fragmentation, stale statistics, or data volume outpacing the current query plan. When those reports feed regulatory filings with hard deadlines, the risk isn't just operational — it's compliance exposure.

Recurring Manual Intervention

When DBAs are repeatedly killing long-running queries, manually clearing locks, or restarting services to maintain stability, firefighting has replaced maintenance. At that point, a reactive patch won't hold — the database needs a structured diagnostic and tuning review.

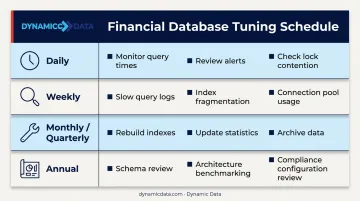

Database Performance Tuning Schedule for Financial Services

Financial databases can rarely afford maintenance windows during market or business hours. That constraint shapes everything — tuning activities must fit around trading sessions, batch processing cycles, and regulatory reporting deadlines rather than generic IT schedules.

| Cadence | Key Activities |

|---|---|

| Daily | Monitor query execution times and resource utilization; review automated alerts; check for lock contention during off-peak hours |

| Weekly | Review slow query logs; identify top resource-consuming queries; check index fragmentation levels; verify connection pool usage |

| Monthly/Quarterly | Rebuild fragmented indexes; update database statistics; review partitioning strategy; archive historical data; validate indexing strategy against current query patterns |

| Annual | Full schema and data model review; benchmark against prior-year baseline; evaluate architecture fit for projected growth; review compliance and security configurations for new regulatory requirements |

Environment-Specific Considerations

- High-frequency trading environments require near-real-time performance monitoring with automated alerting — manual review cadences aren't sufficient at that scale

- Retail banking databases typically align maintenance windows with overnight batch processing cycles, where impact on live operations is minimized

The right cadence reduces firefighting. Teams that schedule proactive tuning around these rhythms spend less time responding to production incidents and more time on structural improvements.

Conclusion

Database performance tuning in financial services is a continuous discipline. The institutions that treat it as a strategic priority — with defined cadences, proactive monitoring, and architectural decisions made with performance in mind — are the ones that consistently deliver reliable customer experiences, meet regulatory obligations, and maintain competitive positioning as data volumes grow.

The path forward is clear: start with query optimization and indexing (highest impact, fastest returns), establish a tuning schedule that fits your operational rhythm, and monitor proactively rather than reacting to incidents.

For organizations facing data volume pressure on transactional databases, the deeper fix is architectural. Working with a data engineering partner like Dynamic Data to build a properly structured modern data stack — routing analytical workloads to platforms like Snowflake or BigQuery — keeps those queries off your live transaction systems entirely, resolving the structural problem rather than managing around it.

Frequently Asked Questions

What is database performance tuning?

Database performance tuning is the process of optimizing a database system's configuration, queries, indexes, and resource allocation to improve speed, reliability, and efficiency. In financial services, this is especially critical — data access speeds directly affect trade execution, fraud detection, customer experience, and regulatory compliance.

What techniques do you use for database performance tuning?

The core techniques include:

- Query optimization and strategic indexing

- Data partitioning and connection pooling

- Caching and resource configuration

The right combination depends on workload type — transactional systems prioritize low-latency writes and reads, while analytical systems benefit more from partitioning and columnar storage.

How do you optimize a data model for performance?

Data model optimization means structuring tables to minimize unnecessary joins, applying the right normalization level for the use case (star schema suits analytical workloads well), and aligning the model with the most frequent query patterns. Regular review matters because query behavior shifts as business needs change.

What is the best database for financial data?

The right database depends on the use case. OLTP systems (PostgreSQL, SQL Server, Oracle) handle transactional workloads; columnar databases (Snowflake, Redshift, BigQuery) suit analytics and reporting; time-series databases handle market data feeds. Most financial institutions run a combination of all three.

How often should financial databases be performance tuned?

Financial databases require continuous tuning — daily monitoring, weekly query and index reviews, monthly or quarterly deeper maintenance, and annual architecture assessments. Data volumes and query patterns shift with business growth, so a one-time tuning exercise degrades quickly without ongoing attention.

What are the biggest performance risks for financial databases?

The most common risks include:

- Unoptimized queries on high-volume transactional tables

- Index fragmentation building up over time

- Latency from legacy system integrations

- Compliance and security overhead consuming database resources

- Insufficient capacity planning for peak periods like quarter-end reporting or market open/close surges